비트코인시세예측

in Study on datavisualization

비트코인 시세 예측하기

# -*- coding: utf-8 -*-

%matplotlib inline

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings("ignore")

# Data Source : https://www.blockchain.com/ko/charts/market-price?timespan=60days

file_path = 'data/market-price.csv'

bitcoin_df = pd.read_csv(file_path, names = ['day', 'price'])

# 기본 정보를 출력

print(bitcoin_df.shape)

print(bitcoin_df.info())

#칼럼은 날짜와가격

(365, 2)

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 365 entries, 0 to 364

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 day 365 non-null object

1 price 365 non-null float64

dtypes: float64(1), object(1)

memory usage: 5.8+ KB

None

bitcoin_df.tail()

| day | price | |

|---|---|---|

| 360 | 2018-08-22 00:00:00 | 6575.229167 |

| 361 | 2018-08-23 00:00:00 | 6434.881667 |

| 362 | 2018-08-24 00:00:00 | 6543.645714 |

| 363 | 2018-08-25 00:00:00 | 6719.429231 |

| 364 | 2018-08-26 00:00:00 | 6673.274167 |

# to_datetime으로 day 피처를 시계열 칼럼으로 변환

bitcoin_df['day'] = pd.to_datetime(bitcoin_df['day'])

# day 데이터프레임의 index로 설정 (시각화 하기 쉽다)

bitcoin_df.index = bitcoin_df['day']

bitcoin_df.set_index('day', inplace=True)

bitcoin_df.head()

| price | |

|---|---|

| day | |

| 2017-08-27 | 4354.308333 |

| 2017-08-28 | 4391.673517 |

| 2017-08-29 | 4607.985450 |

| 2017-08-30 | 4594.987850 |

| 2017-08-31 | 4748.255000 |

bitcoin_df.describe()

| price | |

|---|---|

| count | 365.000000 |

| mean | 8395.863578 |

| std | 3239.804756 |

| min | 3319.630000 |

| 25% | 6396.772500 |

| 50% | 7685.633333 |

| 75% | 9630.136277 |

| max | 19498.683333 |

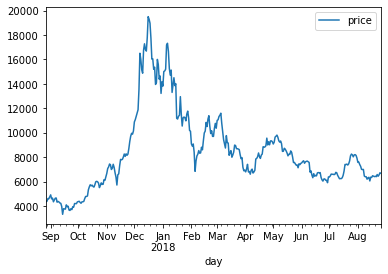

# 일자별 비트코인 시세를 시각화

bitcoin_df.plot()

plt.show()

ARIMA를 활용한 시세 예측

# ARIMA 모델 활용하기

from statsmodels.tsa.arima_model import ARIMA

import statsmodels.api as sm

# (AR=2, 차분=1, MA=2) 파라미터로 ARIMA 모델을 학습

model = ARIMA(bitcoin_df.price.values, order=(2,1,2))

model_fit = model.fit(trend='c', full_output=True, disp=True)

print(model_fit.summary())

ARIMA Model Results

==============================================================================

Dep. Variable: D.y No. Observations: 364

Model: ARIMA(2, 1, 2) Log Likelihood -2787.553

Method: css-mle S.D. of innovations 512.415

Date: Tue, 26 Jan 2021 AIC 5587.107

Time: 17:18:43 BIC 5610.490

Sample: 1 HQIC 5596.400

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 6.1416 27.794 0.221 0.825 -48.334 60.618

ar.L1.D.y -0.3790 1.829 -0.207 0.836 -3.964 3.206

ar.L2.D.y 0.1585 1.192 0.133 0.894 -2.178 2.495

ma.L1.D.y 0.4571 1.825 0.250 0.802 -3.120 4.034

ma.L2.D.y -0.1940 1.339 -0.145 0.885 -2.819 2.431

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -1.5864 +0.0000j 1.5864 0.5000

AR.2 3.9777 +0.0000j 3.9777 0.0000

MA.1 -1.3797 +0.0000j 1.3797 0.5000

MA.2 3.7354 +0.0000j 3.7354 0.0000

-----------------------------------------------------------------------------

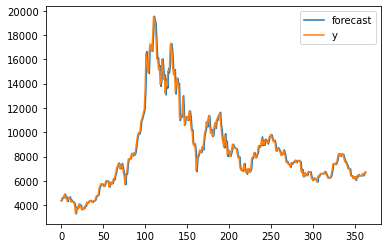

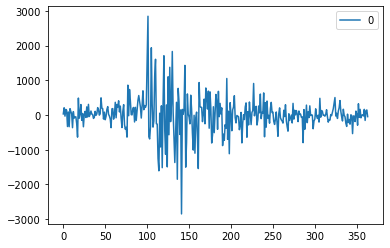

# 모델의 성능 & 예측 결과 시각화

fig = model_fit.plot_predict() # 학습 데이터에 대한 예측 결과 (첫번째 그래프)

residuals = pd.DataFrame(model_fit.resid) # 잔차의 변동을 시각화 (두번째 그래프)

residuals.plot()

<matplotlib.axes._subplots.AxesSubplot at 0x26e2442b190>

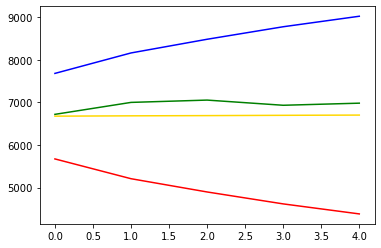

예측 결과인 마지막 5일의 예측값을 실제 데이터와 비교

# 예측 결과인 마지막 5일의 예측값을 실제 데이터와 비교

forecast_data = model_fit.forecast(steps=5) # 학습 데이터셋으로부터 5일 뒤를 예측

# 테스트 데이터셋을 불러옵니다.

test_file_path = 'data/market-price-test.csv' # 실제데이터

bitcoin_test_df = pd.read_csv(test_file_path, names=['ds', 'y'])

pred_y = forecast_data[0].tolist() # 마지막 5일의 예측 데이터입니다. (2018-08-27 ~ 2018-08-31)

test_y = bitcoin_test_df.y.values # 실제 5일 가격 데이터입니다. (2018-08-27 ~ 2018-08-31)

pred_y_lower = [] # 마지막 5일의 예측 데이터의 최소값입니다.

pred_y_upper = [] # 마지막 5일의 예측 데이터의 최대값입니다.

for lower_upper in forecast_data[2]:

lower = lower_upper[0]

upper = lower_upper[1]

pred_y_lower.append(lower)

pred_y_upper.append(upper)

plt.plot(pred_y, color="gold") # 모델이 예상한 가격 그래프

plt.plot(pred_y_lower, color="red") # 모델이 예상한 최소가격 그래프

plt.plot(pred_y_upper, color="blue") # 모델이 예상한 최대가격 그래프

plt.plot(test_y, color="green") # 실제 가격 그래프

[<matplotlib.lines.Line2D at 0x26e244dc3d0>]

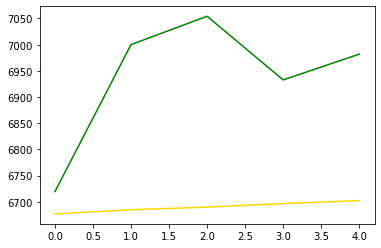

plt.plot(pred_y, color="gold") # 모델이 예상한 가격 그래프

plt.plot(test_y, color="green") # 실제 가격 그래프

[<matplotlib.lines.Line2D at 0x26e24534910>]

from sklearn.metrics import mean_squared_error, r2_score

from math import sqrt

rmse = sqrt(mean_squared_error(pred_y, test_y))

print(rmse)

#test RMSE 점수 : 271.38881165460765

271.38881165460765

Facebook Prophet 활용하기

from fbprophet import Prophet

Importing plotly failed. Interactive plots will not work.

# prophet을 사용하기 위해서는 다음과 같이 피처의 이름을 변경해야 : 'ds', 'y'

bitcoin_df = pd.read_csv(file_path, names=['ds', 'y'])

prophet = Prophet(seasonality_mode='multiplicative',

yearly_seasonality=True,

weekly_seasonality=True, daily_seasonality=True,

changepoint_prior_scale=0.5)

prophet.fit(bitcoin_df)

<fbprophet.forecaster.Prophet at 0x26e283e0b80>

# 5일을 내다보며 예측

future_data = prophet.make_future_dataframe(periods=5, freq='d')

forecast_data = prophet.predict(future_data)

forecast_data.tail(5)

| ds | trend | yhat_lower | yhat_upper | trend_lower | trend_upper | daily | daily_lower | daily_upper | multiplicative_terms | ... | weekly | weekly_lower | weekly_upper | yearly | yearly_lower | yearly_upper | additive_terms | additive_terms_lower | additive_terms_upper | yhat | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 365 | 2018-08-27 | 738.543896 | 6226.354661 | 7523.184197 | 738.543896 | 738.543896 | 9.563964 | 9.563964 | 9.563964 | 8.374726 | ... | -0.006602 | -0.006602 | -0.006602 | -1.182636 | -1.182636 | -1.182636 | 0.0 | 0.0 | 0.0 | 6923.647020 |

| 366 | 2018-08-28 | 742.612648 | 6331.158178 | 7684.153133 | 742.612648 | 742.612648 | 9.563964 | 9.563964 | 9.563964 | 8.452304 | ... | 0.019974 | 0.019974 | 0.019974 | -1.131634 | -1.131634 | -1.131634 | 0.0 | 0.0 | 0.0 | 7019.400574 |

| 367 | 2018-08-29 | 746.681400 | 6309.449564 | 7769.245266 | 745.975687 | 746.681400 | 9.563964 | 9.563964 | 9.563964 | 8.421478 | ... | -0.046634 | -0.046634 | -0.046634 | -1.095851 | -1.095851 | -1.095851 | 0.0 | 0.0 | 0.0 | 7034.842537 |

| 368 | 2018-08-30 | 750.750152 | 6359.511516 | 7822.480347 | 742.394998 | 752.714854 | 9.563964 | 9.563964 | 9.563964 | 8.468117 | ... | -0.017649 | -0.017649 | -0.017649 | -1.078198 | -1.078198 | -1.078198 | 0.0 | 0.0 | 0.0 | 7108.190099 |

| 369 | 2018-08-31 | 754.818904 | 6392.727069 | 7958.671178 | 738.744214 | 768.244440 | 9.563964 | 9.563964 | 9.563964 | 8.518827 | ... | 0.035872 | 0.035872 | 0.035872 | -1.081008 | -1.081008 | -1.081008 | 0.0 | 0.0 | 0.0 | 7184.990775 |

5 rows × 22 columns

forecast_data[['ds', 'yhat', 'yhat_lower', 'yhat_upper']].tail(5)

| ds | yhat | yhat_lower | yhat_upper | |

|---|---|---|---|---|

| 365 | 2018-08-27 | 6923.647020 | 6226.354661 | 7523.184197 |

| 366 | 2018-08-28 | 7019.400574 | 6331.158178 | 7684.153133 |

| 367 | 2018-08-29 | 7034.842537 | 6309.449564 | 7769.245266 |

| 368 | 2018-08-30 | 7108.190099 | 6359.511516 | 7822.480347 |

| 369 | 2018-08-31 | 7184.990775 | 6392.727069 | 7958.671178 |

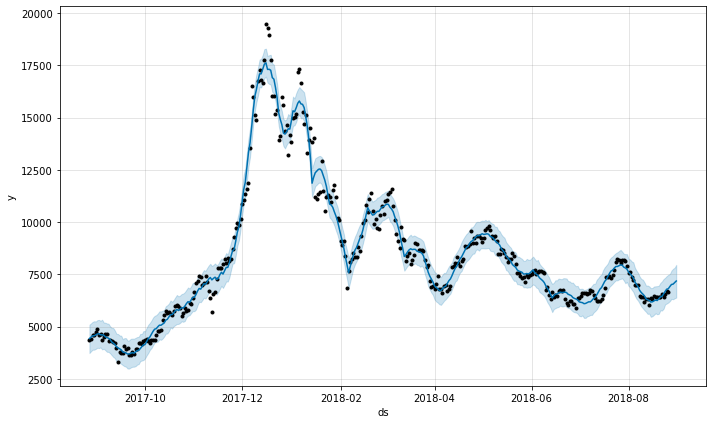

#전체 데이터를 기반으로 학습한, 5일 단위의 예측 결과를 시각화

fig1 = prophet.plot(forecast_data)

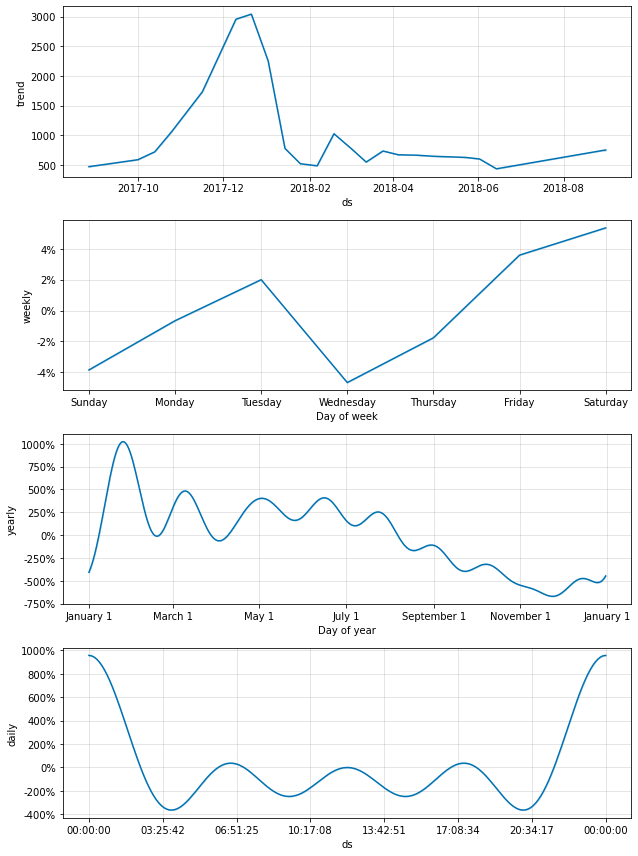

# seasonality_mode로 설정했었던 기간별 트렌드 정보를 시각화

fig2 = prophet.plot_components(forecast_data)

실제 데이터와의 비교

bitcoin_test_df = pd.read_csv(test_file_path, names=['ds', 'y'])

pred_y = forecast_data.yhat.values[-5:] # 마지막 5일의 예측 데이터입니다. (2018-08-27 ~ 2018-08-31)

test_y = bitcoin_test_df.y.values # 실제 5일 가격 데이터입니다. (2018-08-27 ~ 2018-08-31)

pred_y_lower = forecast_data.yhat_lower.values[-5:] # 마지막 5일의 예측 데이터의 최소값

pred_y_upper = forecast_data.yhat_upper.values[-5:] # 마지막 5일의 예측 데이터의 최대값

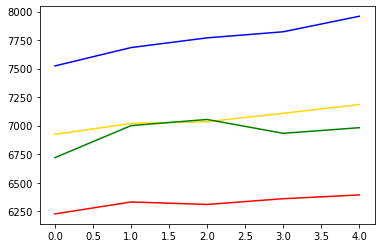

plt.plot(pred_y, color="gold") # 모델이 예상한 가격 그래프

plt.plot(pred_y_lower, color="red") # 모델이 예상한 최소가격 그래프

plt.plot(pred_y_upper, color="blue") # 모델이 예상한 최대가격 그래프

plt.plot(test_y, color="green") # 실제 가격 그래프

[<matplotlib.lines.Line2D at 0x26e2ae87be0>]

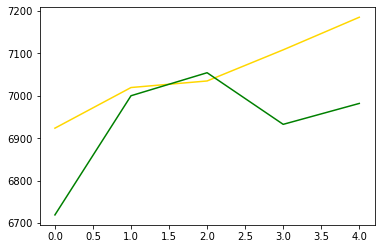

plt.plot(pred_y, color="gold") # 모델이 예상한 가격 그래프

plt.plot(test_y, color="green") # 실제 가격 그래프

[<matplotlib.lines.Line2D at 0x26e2ae51940>]

rmse = sqrt(mean_squared_error(pred_y, test_y))

print(rmse)

# test RMSE 점수 : 151.367832019998

151.367832019998